by Roel Aerts

Greystone Logistics (GLGI) designs and manufactures plastic pallets for the logistics trade. They use recycled plastic which might in any other case be destined for landfill. They grind and pelletize the plastic in home. Injection molding and proprietary resin mix is used to fabricate the pallets.

Greystone is headquartered in Oklahoma and has its manufacturing plant in Iowa.

Latest outcomes and Financials

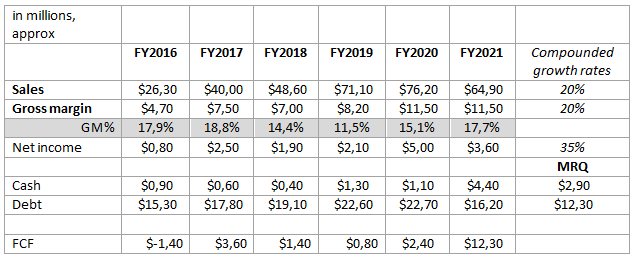

· The corporate had invested closely in manufacturing tools a number of years in the past, that loaded them with fairly some debt. During the last years they labored on a large discount in debt. In 2 years they diminished it from 21.6M$ to 9.4M$ at the moment (debt minus money).

· Very excessive free money circulation technology in fiscal 2021, 12M$. At this tempo they theoretically might be debt free finish 2022 in the event that they select to be.

· Gross margins of ~17% or greater from 2020 onwards (except for final quarter). This was the impact of the investments in manufacturing tools. With out being an issue professional, that feels like a really excessive margin for a pallet, a commodity to me.

· Excessive progress, 20% compounded progress in gross sales and gross margin from 2016 until 2020, 35% compounded progress in earnings. Shrinking numbers in FY2021. Can they decide up the expansion path?

· Potential for diminished bills in calendar yr 2022, near 1,000,000 in curiosity funds vs. 2021 ought to they repay the vast majority of debt, and several other 100k$ in leases that run at decrease lease value of their final yr.

· Final reported quarter, ending August 31 2021, was weaker than earlier ones. Administration attributes this to scarcity of personnel within the COVID restoration and downtime on manufacturing machines. Driving down margins as properly.

Outlook, progress alternatives

· Can they decide up the expansion path from 2016 to 2020? Their excessive free cashflow ought to give them room to put money into progress. Progress stagnated and fell again in FY2021 and first quarter of FY2022. World pallet market is forecasted to develop ~5% CAGR within the subsequent years, nonetheless, Greystones progress potential is in prospects that transfer from the omnipresent wood pallets to plastics pallets. That progress price might be, ought to be, a lot greater.

· Attainable beneficiary of a inexperienced tailwind the place prospects need reusable, recycled options, usually pushed by client demand. Rising automation by pallet customers might be progress driver as properly

· “Greystone believes that the demand for its pallets is growing which is primarily anticipated to have a constructive impression on operations over the past half of the present fiscal yr in addition to future years.” (Quarterly report Oct 2021)

Administration, board and buyers

· Plenty of pores and skin within the sport, CEO owns greater than 34% of widespread inventory.

· Second largest shareholder is a Director, along with CEO they every personal 50% of the popular shares, they management the board.

Wonderful multiples (TTM):

· P/S 0.4

· P/E 4.2

· P/FCF 2.5

Dangers

· Nano-cap, solely 24M$ valuation, with corresponding dangers related

· Excessive buyer focus, lower than 5 prospects account for greater than 80% of income. There was gradual enchancment over the previous years. Dangers related to most small-caps.

· Management of the board by 2 individuals. Are their pursuits aligned with widespread shareholders? Excessive insider possession is often a great factor; for micro-caps, whole management by insiders is one thing to look at. How to make sure they don’t use the corporate as their personal financial institution? (cf. Leases and loans administrators have excellent to the corporate; however these appear honest valued and restricted in time, no indicators this danger is materializing.)

Questions

· At what capability degree are they working?

Conclusion

This seems to be like a price play from the FY2021 numbers, however it might be an rising progress story in the event that they go attempt to decide up the expansion path they have been on in 2016-2020.

DISCLOSURE: Lengthy GLGI

Concerning the writer:

Roel Aerts is a retail investor with a give attention to renewables and clear expertise. Insights and analyses above are written for his personal functions and are shared to assist others type an opinion and to assemble suggestions. It isn’t meant as funding recommendation and Roel just isn’t an funding advisor. Roel holds a grasp’s diploma in Electrical Engineering and in Industrial Administration.

0 Comments